The employment conundrum continues

Raymond James Chief Economist Eugenio J. Alemán discusses current economic conditions.

North is south, south is west, west is east, east is north, up is down, and down is steady. This week’s employment reports have something for everyone, which is precisely why we should interpret them cautiously. Political and economic commentators will inevitably try to fit the data into their preferred narrative, but drawing conclusions from a single month of numbers is a mistake.

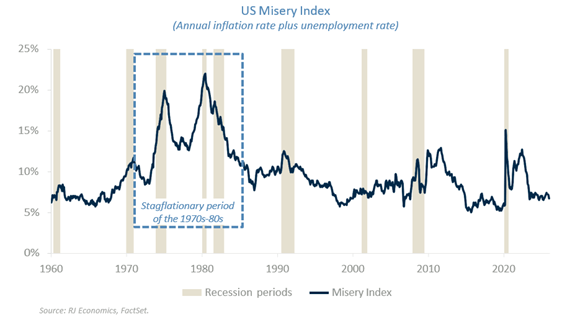

Some analysts will undoubtedly revive talk of “stagflation,” leaning on superficial historical comparisons to the 1970s, particularly given Iran’s involvement in the current geopolitical environment. A few months ago, we even had to address a separate claim that the US is destined for a 2030s depression simply because we experienced one in the 1930s. Yes, “history repeats itself,” but the economic and institutional conditions underlying those historical periods were so fundamentally different that such parallels are not meaningful.

To be clear: This is not a return to 1970s-80s stagflation.

As we discuss below, the US economy is currently growing above potential, which rules out the “stagnation” component of stagflation. Inflation is indeed above the Fed’s 2% target, but nowhere near the levels of that era. Neither growth nor inflation resembles the stagflation environment of the 1970s-80s.

Fed policy: Watching headline versus core inflation

Despite rising political noise, the Federal Reserve remains independent and is not at risk of lowering interest rates due to political pressure. While markets may react to the employment report by pricing in more aggressive rate cuts, we still expect only one rate cut this year. The Fed is unlikely to respond to a single month of data, especially with gasoline prices expected to push headline inflation higher in coming months.

Fed officials will be closely watching the gap between headline inflation, which includes food and energy, and core inflation, which excludes food and energy.

If core inflation begins to track higher along with headline inflation, rate cuts are likely off the table. If instead only headline inflation rises while core readings remain stable, and if employment weakens further, rate reductions could still occur.

For context, job growth was 126,000 in January and -92,000 in February, averaging 17,000 per month so far this year, slightly above last year’s monthly average. At this stage, there is limited evidence that labor market conditions have deteriorated meaningfully beyond last year’s slowdown.

Are the ISMs showing the path forward?

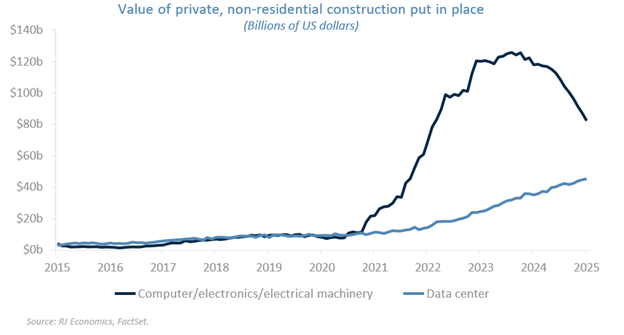

For the first time since 2023, the US economy appears to be gaining momentum across sectors. The manufacturing sector in particular has shown signs of life, posting two consecutive expansionary readings in the ISM Manufacturing PMI. While many observers credit the AI boom, the underlying driver is more structural: the CHIPS Act and the Inflation Reduction Act, which triggered a surge in manufacturing construction starting in 2021. These investments are now coming online. More recently, data center construction – boosted by AI-related demand – has added further momentum.

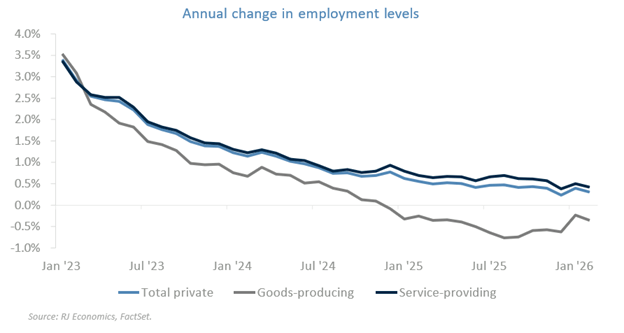

Yet, this manufacturing rebound has not translated into job creation. Employment in the sector has continued to decline since mid-2025 due to elevated input costs driven by tariffs. While overall activity has expanded this year, pricing pressures jumped in February and manufacturing employment remained negative, signaling that the sector is improving but not fully healed.

On the services side, growth strengthened in February while price pressures eased versus January. Service sector employment also firmed modestly.

Putting it all together

With contradictory signals emerging early in the year, it is essential to step back and view the full mosaic of data rather than cherry picking one number. For example, the control group retail sales series showed solid growth in January, and although February may be weather affected, consumer demand remains healthy, driven more by wealth accumulation than by income gains.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.